Oreninc Index Update: August 21, 2017

ORENINC INDEX falls as vacation season continues

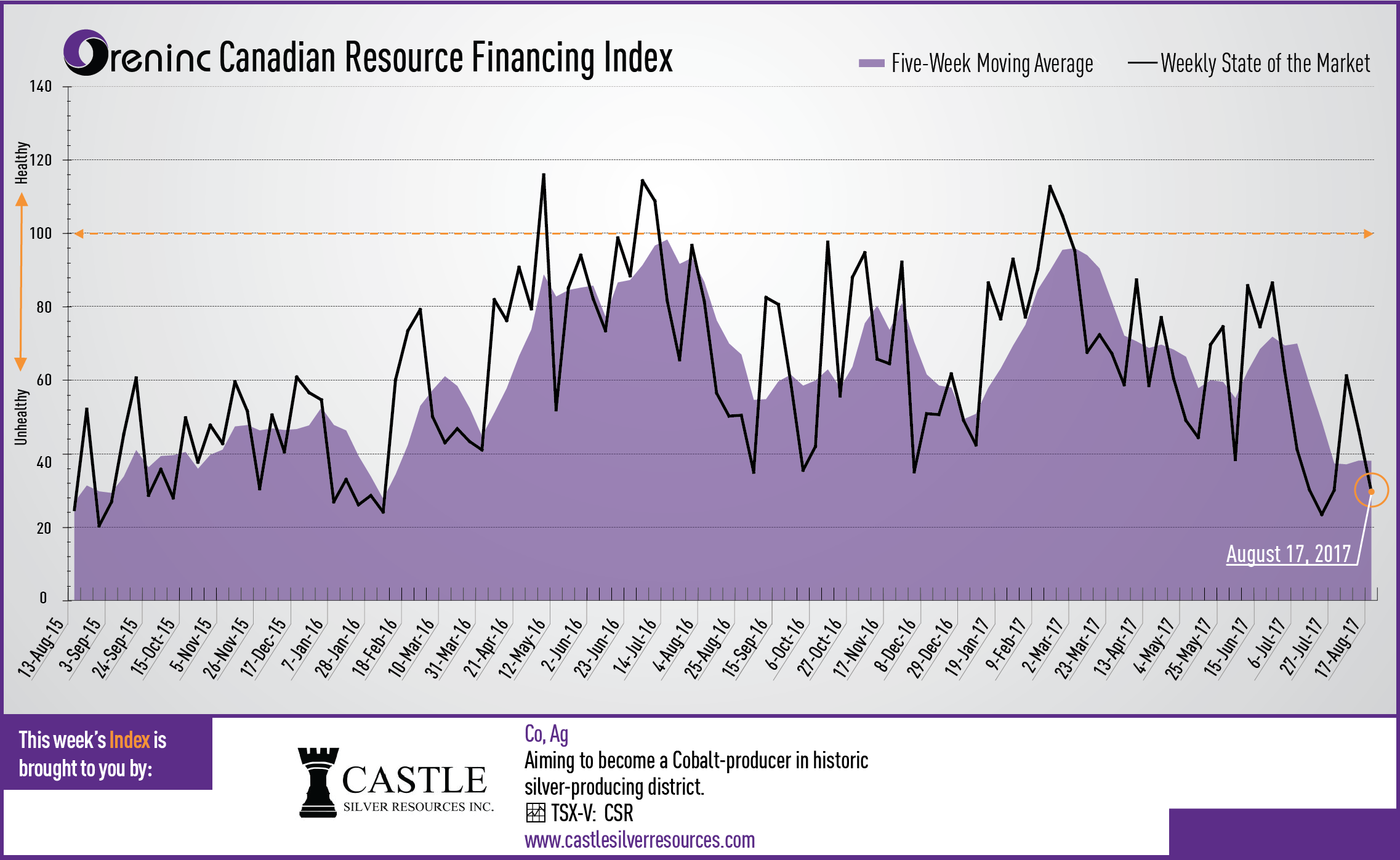

ORENINC INDEX - Monday, August 21th, 2017

North America’s leading junior mining finance data provider

Follow us on facebook and find us on Twitter @Oreninc

Last week index score: 46.26

This week: 29.82

The Oreninc Index fell in the week ending August 18th, 2017 to 29.82 from 46.26 the previous week with the markets very quiet as vacation season continues. The index is a little odd this week as it is down although several of the metrics increased, the reason being the lack of brokered deals this week and the four-day trading week last week that artificially boosted last week’s score. In addition, many open deals extended their closing dates.

Total fund raises announced increased to C$45.3 million, a two-week high, which included one brokered financing for C$4.2 million, a four-week low, and no bought-deal financings. The average offer size grew to C$2.1 million, a six-week high, whilst the total number of financings announced increased to 22, a two-week high.

On the political front, omissions can have far-reaching consequences as US president Donald Trump is find out. His failure to speak out against a white supremacist rally in Virginia has seen an exodus of business leaders from his CEO think-tanks (prompting him to close them) and being able to do what most presidents cannot: see Republicans and Democrats unite in non-partisan agreement on an issue. Interestingly, markets reacted more to this Trump news than about the puerile bellicose exchange the previous week with North Korea.

Despite relatively low levels of activity, gold had an interesting and strong week including briefly breaking through the US$1,300/oz mark, benefitting from mixed opinions among members of the Federal Open Market Committee on inflation and future interest rate hikes, which were interpreted to mean that future rate hikes will come later rather than sooner. Gold also benefitted from flight-to-safety moves as the stock market sold off as attention focused on the US president.

Gold closed the week at US$1,284/oz down slightly from US$1,289 last week. The van Eck managed GDXJ also retrenched slightly and is now up 5.8% so far in 2017 at US$33.39. The recently launched US Global Go Gold ETF posted gains to close at US$12.43 from US$12.40 last week, whilst the inventory of the SPDR GLD ETF poseted gains to close the week at 799 tonnes from 787 tonnes the previous week.

In other commodities, silver bounced over and below the US$17/oz mark and closed just under at US$16.98/oz from US$17.11/oz. The Comex copper price continues to hover just under the US$3/lb level and closed up at US$2.96/lb from US$2.91/lb the previous week. Zinc is on a charge with the LME price breaking through the US$3,000/t level to close at US$3,124/t from US$2,896/t a week ago. Oil spent most of the week falling but recovered at week end to close slightly down at US$48.51 per barrel from US$48.82 per barrel last week.

The markets had enough of Trump’s guff this week, prompting a late-week sell-off that saw the Dow Jones Industrial Average fall to 21,674 from 21,858 last week. Canada’s S&P/TSX Composite Index mirrored the DJIA chart and also saw a late week sell-off to close down below 15,000 at 14,952 from 15,033 the previous week. The S&P/TSX Venture Composite Index increased to close at 769.76 from 762.81 the previous week.

Summary:

- Number of financings increased to 22, a 2-week high.

- One brokered financings were announced this week for $4.2m, a 4-week low.

- No bought-deal financings were announced this week, an eleven-week low.

- Total dollars grew to $45.3m, a 2-week high.

- Average offer size also grew to $2.1m, a 6-week high.

Financial news highlights

Almonty Industries (TSXV: AII) opened and closed a C$6.4 million with its president & CEO Lewis Black to subscribe for 21.2 million shares @ C$0.30.

- Upon closing Black holds 36.5 million shares representing about 22.55% of the issued and outstanding stock.

- Proceeds will be used for the equity portion of the development financing necessary for the Sangdong mine project in China

- Sangdong was historically one of the largest tungsten mines in the world and was acquired in September 2015 through the acquisition of Woulfe Mining

Orosur Mining (TSX: OMI) announced a financing to raise C$4.0 million through a placement of 16.7 million shares @ C$0.24.

- The subscription was oversubscribed

- Each subscription includes a warrant exercisable @ C$0.337 for three years

- The net proceeds are to be used for drilling the Anzá gold project in Colombia

Major Financing Openings:

- Ikkuma Resources (TSXV: IKM) opened a C$10.00 million offering on a best efforts basis. The deal is expected to close on or about September 1st.

- Almonty Industries (TSXV: AII) opened a C$6.35 million offering on an insider only basis.

- Orosur Mining (TSXV: OMI) opened a C$4.20 million offering underwritten by a syndicate led by Numis Securities on a best efforts basis. Each unit includes half a warrant that expires in 36 months.

- American CuMo Mining (TSXV: MLY) opened a C$3.75 million offering on a best efforts basis. Each unit includes a warrant that expires in 24 months.

Major Financing Closings:

- Red Eagle Mining (TSX: R) closed a C$29.96 million offering on a best efforts basis. Each unit included a warrant that expires in 60 months.

- Peregrine Diamonds (TSX: PGD) closed a C$10.28 million offering on a best efforts basis.

- Almonty Industries (TSXV: AII) closed a C$$6.35 million offering on a insiders only basis.

- GT Gold (TSXV: GT) closed a C$5.75 million offering underwritten by a syndicate led by Haywood Securities on a best efforts basis.

Comments