Oreninc Index: May 6, 2019

ORENINC INDEX up as financings and brokered deals return

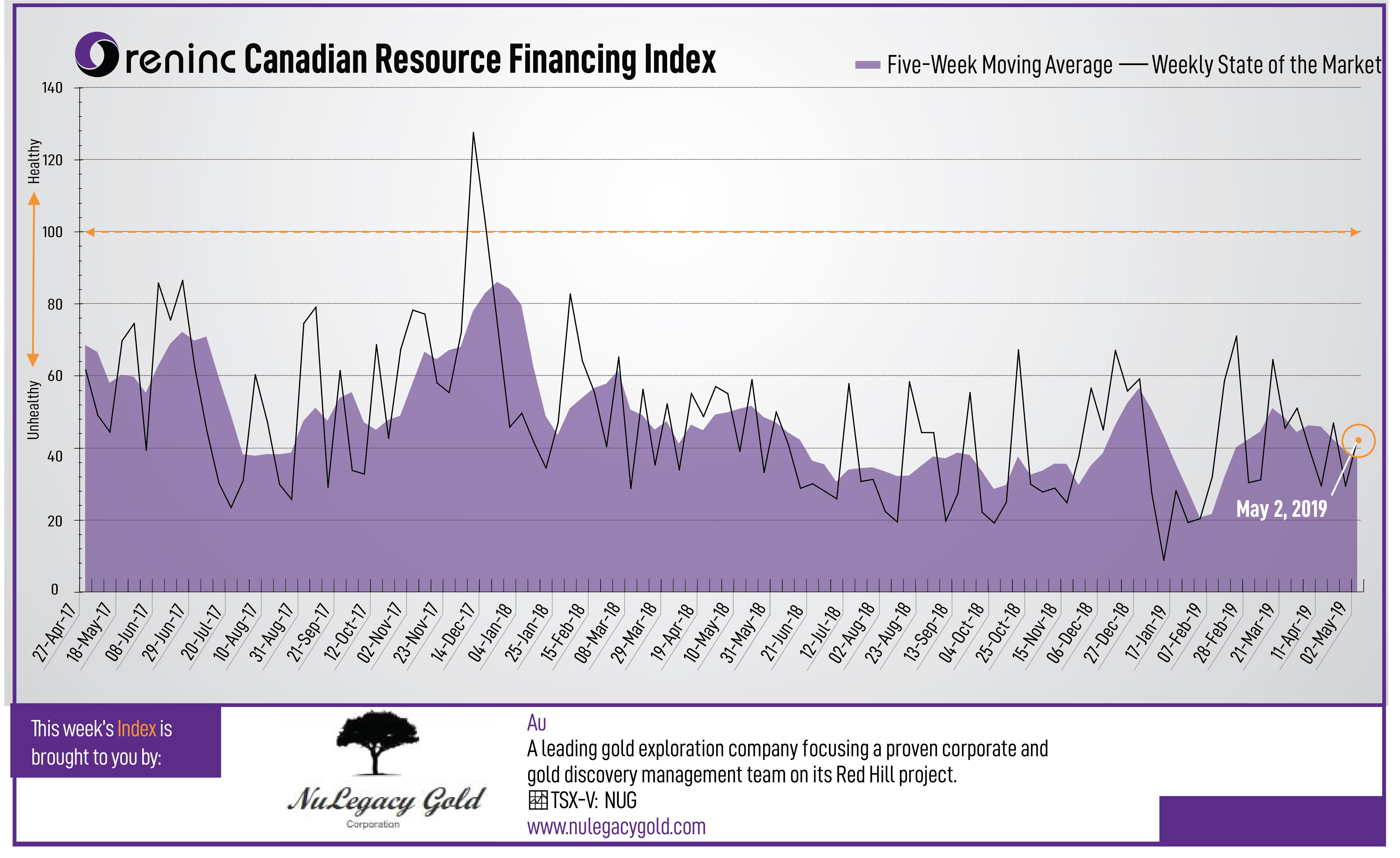

ORENINC INDEX - Monday, May 6th 2019

North America’s leading junior mining finance data provider

Sign up for our free newsletter at www.oreninc.com

Last week index score: 29.36

This week: 42.67

The Oreninc Index bounced back the week May 3rd, 2019 to 42.67 from 29.36 a week ago as financial action and brokered deals returned to the market.

A tough week for gold, which fell to its lowest point of the year as US Federal Reserve chairman Jerome Powell cast doubt on the idea of a near-term reduction in interest rates. However, gold is proving to be resilient, with the World Gold Council reporting that central banks bought 145.5 tonnes of yellow metal in the first quarter, 68% more than in the same period last year. As the week ended, gold shrugged-off a stronger than expected US non-farm payrolls data from the US Labor Department, which a 263,000 rise in April, while the unemployment rate fell to a 49-year low of 3.6%, all of which sees gold continue to be range-bound. Gold stocks, however, continue to be sold off.

On the geopolitical front, US trade negotiations with China continue to advance and US president Donald Trump extended an olive branch of positive comments about his North Korean counterpart Kim Jong-Un despite the Asian nation conducting more short-range missile tests.

The possibility of the United Kingdom (UK) leaving the European Unions continues to wreak havoc in UK politics with the ruling Conservative party suffering a wave of defeats in local elections. Attempts by prime minister Teresa May to reach a deal with the opposition counterpart Jeremey Corbin have been widely opposed by parliamentarians from both sides of the House. So, the net takeaway is that there is still no clarity about what—if anything—will happen come October when the UK extension to the Article 50 process expires.

Before that, later this month will see the European Parliamentary elections in which the UK will participate. Many expect the Conservatives to lose more ground and those factions that support the UK leaving the EU to do well. Time will tell.

On to the money: total fund raises announced increased to C$71.3 million, a two-week high, that included two brokered financings and for C$16.5 million, a five-week high, and no bought-deal financings. The average offer size increased to C$2.6 million, a seven-week high, whilst the number of financings increased to 27, a two-week high.

Another fight-back late in the week capped another losing week for gold as it closed down at US$1,279/oz from US$1,286/oz a week ago. The yellow metal is down 0.26% so far this year. The US dollar index pulled back a little as it down up at 97.52 from 98.00 last week. The van Eck managed GDXJ sold off again as it closed down at US$28.41 from US$30.12 a week ago. The index is now down 5.99% so far in 2019. The US Global Go Gold ETF also sold off as it closed down at US$11.56 from US$12.22 last week. It is up 1.32% so far in 2019. The HUI Arca Gold BUGS Index followed suit and closed down at 152.99 from 160.47 last week. The SPDR GLD ETF continued to sell off as its inventory closed down at 740.82 tonnes from 746.69 tonnes a week ago. It was last at these inventory levels in October 2018.

In other commodities, silver fell below the US$15/oz level again as it closed down at US$14.94/oz from US$15.09/oz a week ago. Copper also continued to shed cents as it closed down at US$2.81/lb from US$2.89/lb a week ago. Oil returned to winning ways as WTI closed up at US$61.94 a barrel from US$63.30 a barrel a week ago.

The Dow Jones Industrial Average ticked down slightly as it closed down at 26,504 from 26,543 last week. Canada’s S&P/TSX Composite Index it closed down at 16,494 from 16,613 the previous week. The S&P/TSX Venture Composite Index closed down at 606.42 from 610.69 last week.

Summary

· Number of financings increased to 27, a two-week high.

· 2 brokered financings were announced this week for $16.5m, a five-week high.

· No bought-deal financings were announced this week, a two-week low.

· Total dollars heightened to $71.3m, a two-week high.

· Average offer up to $2.6m, a seven-week high.

Financing Highlights

Thor Explorations (TSXV:THX) opened a private placement of up to 100.5 million shares @ C$0.20 for aggregate gross proceeds of up to C$20.0 million.

· The net proceeds will be used to develop the Segilola gold project in Nigeria and further exploration in Nigeria and at the Douta project in Senegal.

Major Financing Openings

· Thor Explorations (TSXV:THX) opened a C$20.1 million offering on a best efforts basis.

· Ascot Resources (TSXV:AOT) opened a C$10.0 million offering underwritten by a syndicate led by Sprott Capital Partners on a best efforts basis.

· Royal Road Minerals (TSXV:RYR) opened a C$8.0 million offering underwritten by a syndicate led by Pollitt & Co. on a best efforts basis.

· First Mining Gold (TSX:FF) opened a C$6.01 million offering on a best efforts basis.

Major Financing Closings

· Sarama Resources (TSXV:SWA) closed a C$5.86 million offering on a best efforts basis.

· Para Resources (TSXV:PBR) closed a C$5.33 million offering on a best efforts basis.

· Maritime Resources (TSXV:MAE) closed a C$3.68 million offering on a best efforts basis.

Comments